Riley Mengarelli started ranching cattle when he was 15. Just a skinny high school freshman, he had already figured he could use the livestock to help pay for college. He bought a few heifers, bred them, and sold their calves at an auction that fall. Then he did the whole thing again the next year.

Now a Washington State University senior, Mengarelli has used his cattle money and scholarships to pay his way through school and graduate without debt. By maintaining the herd and selling the calves, “I’ve made a few thousand a year,” he says.

(Photo Robert Hubner)

Keeping livestock in Toppenish while attending school 200 miles away in Pullman is, to say the least, a challenge. Though his mother and siblings feed the animals when he’s gone, more than once Mengarelli has had to jump in his Jetta (which doesn’t do much for his cowboy image, but has more fuel-economy than a truck) and race home to help.

“I love the work, though,” says Mengarelli, who plans to keep the herd even after college. “Sure it’s stressful to raise cattle,”he says. “But it’s also really gratifying to see healthy calves and to turn them out on green grass.”

To supplement his calf money, Mengarelli works on the family farm in the summer. Like many WSU students before him, he has blended his wits with hard work to pay his way through school without too much trouble to his folks.

Some do the typical—sell blood at the plasma center in Pullman, offer themselves for psychology studies on campus, and find jobs in town.

Others, through time, have been more creative. During the Depression, Peter Kragt hitchhiked 400 miles from his home in Lynden to Pullman. Then he found a vacant lot, had lumber delivered, and in just three days built himself a cabin where he lived quite efficiently for the rest of the term. He recounted his efforts in an essay titled “How I make Both Ends Meet,” which he entered in a campus contest in 1932.

In 1992, when Pullman was in the midst of a housing shortage, WSU sophomores Keven Hupp ’95 and Dan Pearson ’95 bought a 60-foot mobile home for $12,500. They paid $150 a month to rent their lot, which included sewer and water, and they heated it by burning wood they had brought from home. Because both came from farm families, they had a steady supply of meat and canned fruits and vegetables. Their only food expenses were eggs, milk, and bread.

By the time they graduated in 1995, housing was still at a premium in Pullman. The two put a sign in front of their home at noon one Monday and by 7 p.m. they had sold it for $17,500. “We each left Pullman with $8,750 in our pockets instead of a stack of bills,” says Pearson.

Veterinary student Scott Smiley ’05 bought an old school bus from a church for $1,000. He tore out all the seats and cleaned up the interior. Then he added a propane stove and refrigerator as well as a wood stove, bed, and table. He drove it to Pullman and at the start of school knocked on the doors of farmhouses just outside of town to find the right location and landlord. Some people thought it was a cute idea, he says. “Others thought I was crazy.”

PAYING THE WAY

But not everyone can do it on their own. As director of Student Support Services at Washington State University, Francisco Salinas knows students who have blown through their financial aid the first two months of school, some who are juggling two jobs and five classes, and some who are a week away from being evicted from their apartments.

Salinas and his office are on campus to provide one-on-one counseling for first-generation, low-income, and disabled students who are working on their first undergraduate degree. As the first person in his family to finish college, Salinas knows the turf. It isn’t easy if there isn’t someone in your family who has been through this and can tell you what to do, he says.

Fortunately, students find the 30-something administrator approachable. They’re not afraid to admit they’re failing a class or that they don’t have enough to buy groceries. On a day last spring, he coached a young woman with a disability through preparing for a test. The minute she left, another student, this one with money concerns, filled her seat. He was on food stamps and didn’t have enough cash to cover rent. In addition, he was taking a tough class and hadn’t met with his professor to discuss his grades. Salinas urged the student to approach the faculty member. Then they talked about sticking to a budget. Often, Salinas says, the issues of grades and finances are intertwined.

Just down the hall, program coordinator Elizabeth Wolfe picks through stack of returned textbooks that had been loaned out to low-income students during spring semester. As she sets Guidance of Young Children on top of a nutritional science text, she notes that the $7,000 she had to spend on books this year didn’t go very far.

The office suite holds two private counseling offices with large green metal cabinets. The one in the office on the right contains clothes that students can borrow on a confidential basis. The other is filled with food. “If we have a student who comes in and hasn’t eaten for a couple days, that’s where we take them,” says Salinas. “If we have a student who is dealing with the fact that they don’t know how to budget their money or there was a shortfall in a financial aid award, then we look at a long-term strategy. We contact the Community Action Center and see if they’re eligible for food stamps. We try to help them learn to manage their money.”

Each day a river of students flows past and through the Lighty Student Services building, but only a few land at Student Support Services. And the office is there only because the university takes part in two federal programs that target support at certain student populations. “Our challenge is to take those populations and make sure they earn their four-year degree,” says Salinas. He and his colleagues serve a total of 410 students. “But that’s just a small percentage of the total enrollment,” says Salinas.

And what about the rest?

“They are left to fill the gaps themselves,” says Salinas. Sometimes they can do it with scholarships. Often they work. But as the economy changes and tuition and fees rise faster than inflation, it’s probably the middle class families who are going to feel the pinch the most, says Salinas. “That’s who I’m worried about.”

STUCK IN THE MIDDLE

About $20,000 a year. That’s Washington State University’s estimated costs for an in-state undergraduate. That sum includes tuition of nearly $7,000 and mandatory student fees of another $900. It also factors in housing, food, books, and about $1,200 in traveling expenses.

Gone are the days when the in-state school was the affordable alternative, when the state covered most of the costs for an in-state student, and when students could make up the rest with summer jobs and a little help from mom and dad. In the past four years, tuition and fees at Washington’s universities have risen by more than 29 percent, a staggering increase, though according to a recent report from the Washington State Higher Education Coordinating Board, it’s still less than the national average of 34 percent.

If the country is headed for a recession, it could be more bad news for the price of an education. History has shown that during national recessions, states cut back on higher education appropriations and tuition spikes up. And in most cases, states haven’t increased their student aid to meet the need, according to the Chronicle of Higher Education.

Rising costs and their causes are affecting schools country-wide. Many public schools, WSU included, have resorted to borrowing money to build dormitories and student recreation facilities—important lures for recruiting new students to campus, and often necessary improvements. Michael Blim, author and anthropologist, calls this the “expand or die” moment.

In essence, Blim argues, as universities compete for students, the ones with the newer buildings, state-of- the-art technology, and the fresh student facilities will do a better job of luring those traditional students who can pay their way through school.

But in many cases, students end up paying the costs of expansion through their housing and fees. For example, a student fee of $120/semester goes toward paying for more than half the debt of the $86 million renovation of WSU’s Compton Union Building.

It’s a nation-wide phenomenon. According to a recent College Board report, fees are rising faster than tuitions, as much as 11 percent at public four-year schools like WSU.

Sarah Williams is finding creative ways to augment her student loans and pay for her extra costs like class fees and art supplies. In addition to her part-time job answering the help line in the Student Learning Center, she was a nighttime dorm monitor for Cougar Quest, a summer program for 7th–12th graders.

As she heads into her sophomore year this fall, she’ll have some money saved. She’s creating extra cash by making and selling jewelry. Her handcrafted necklaces, mostly made with hemp and beads, are a regular sight at events like the Lentil Festival. And Williams always thinks about how to expand her business. Last year she started offering her jewelry online at an artisan’s site called ETSY. In the spring, she branched out again, bringing her work into Lily Bee’s Consignment Shop on Main Street in Pullman.

But so far, all her efforts don’t cover all her expenses. That’s why she’s borrowing through federal loans.

BORROWER BEWARE

Every dollar counts, says junior Christine Morgan, who met Francisco Salinas her freshman year. She walked out of the library to see him advertising his program for first generation college students. Since then, she has regularly visited his office for financial advice and help applying for scholarships.

Because of her family’s income, she doesn’t qualify for any extra federal support. That has been frustrating, says Morgan. She and her parents have had to take out loans. At the end of her sophomore year, she had debt close to $20,000. At this rate, by the time she’s a senior, it could be more than $60,000, she says. “It’s scary to think about.”

More than half of WSU’s seniors graduated with student loan debt. In 2007, they owed on average $20,000.

A lot of middle income family students are starting to feel the crunch, says Salinas. “The expected cost of attendance and the difference between that with the expected family contributions is leaving a gap.”

Low-cost federal loans and private scholarships don’t always cover it. “They have to work and they have to keep bugging mom and dad for money that mom and dad don’t think they have,” says Salinas. “Often times it’s because they really don’t have it.”

Lending is changing in every sector. Families who would take out bank loans to help their children through school may not have that option in the next few years. And some private student lenders are changing policies or filing for bankruptcy.

To fill the gap between education loans and college costs, some families tap into their home equity. But as housing prices started to fall last year, people ended up owing more on their homes than they were worth and had nothing to borrow against. According to the Project on Student Debt, the mortgage market had been a resource for some student loan companies raising money to make student loans. Now that investors are more nervous about the economic future in real estate, there is less money available.

And then there are the private loans, which are used by about eight percent of WSU’s undergraduate students. These loans are made based on the student’s credit history and have high interest rates. And where predatory lending with home loans is now mainstream news, private student loans may be the next frontier, warn education experts.

It is a bit of a mess right now, says Wayne Sparks, director of the WSU Office of Financial Aid. Grants haven’t kept up with the increase in college costs, and while there are some increases in scholarships, they haven’t matched the increase in need, he says.

The University does take some measures to protect students who are borrowing money. Before a student can apply for a private loan, for example, he is required to fill out the free application for federal loans and grants. “We want to make sure they have exhausted the availability of lower interest loans before turning to a private lender,” says Sparks. At the end of the spring semester, word came out that a new federal law has increased the total amount of low-cost loans a student could receive from $23,000 to $31,000 and ensures loan access even if conditions in the credit market continue to deteriorate.

Even with the help of low-cost loans, this generation of students is facing new challenges. Sparks and his colleagues see a lot of young adults who come to Pullman with very little financial experience and a willingness to accept loans without fully understanding repayment and interest rates. They may have had jobs, but few have ever purchased a car or managed a large sum of money, says Sparks.

In the most extreme cases, WSU’s advisors have seen undergraduates leave campus owing up to $100,000 in student loan debt, particularly when private lenders are used. But to leave owing that much is a rare event, Sparks is quick to point out.

“We tell our students, ‘Live like a college student while you are in college so you don’t have to live like a college student when you graduate,'” says Sparks.

The University’s financial aid office has offered counseling to students to reduce loan indebtedness. In 2004 WSU received an EdFund grant to reach out to freshmen and their families during new student orientation and get them in the right frame of mind about college costs and expenses. They talked about whether you really need a car in Pullman, the benefits of using cash over credit, and the reality that daily lattes and weekly pizzas can add up to thousands each year.

With the right resources, the financial aid office could do more, says Sparks. Some schools are offering brief courses on personal finance and money management. Ohio State University, for example, tries to reach students during their first five weeks of college because that’s when spending habits are set. Other schools call students in when their loan debt starts looking heavy.

Right now, WSU counsels students before they get their first loan and just before the leave. “The good news is our students at WSU have compiled a very good record in terms of repayment,” says Sparks. “That bodes well for future students looking for aid.”

MORE COSTS ARE COMING

Washington State has always had an allure for practical families looking for a good in-state four-year college education at a reasonable price. But as costs keep rising it will be more difficult for students like Melissa Bughi to pay for school through summer work and a part-time job on campus.

Taking money from her folks wasn’t an option, says Bughi. They have a farm to run and her two younger sisters to think of. The only help she accepted was a loan from them for her first housing deposit and some money this year to buy groceries. “I felt if I could do it, I would take the burden off my parents.”

It would have been great to have had everything paid for through college, says Bughi. But maybe having to work and having to figure her way out of financial hardship had its benefits. It forced her to prioritize her classes and be organized with her time. “And I think I did a pretty good job of doing everything well,” she says.

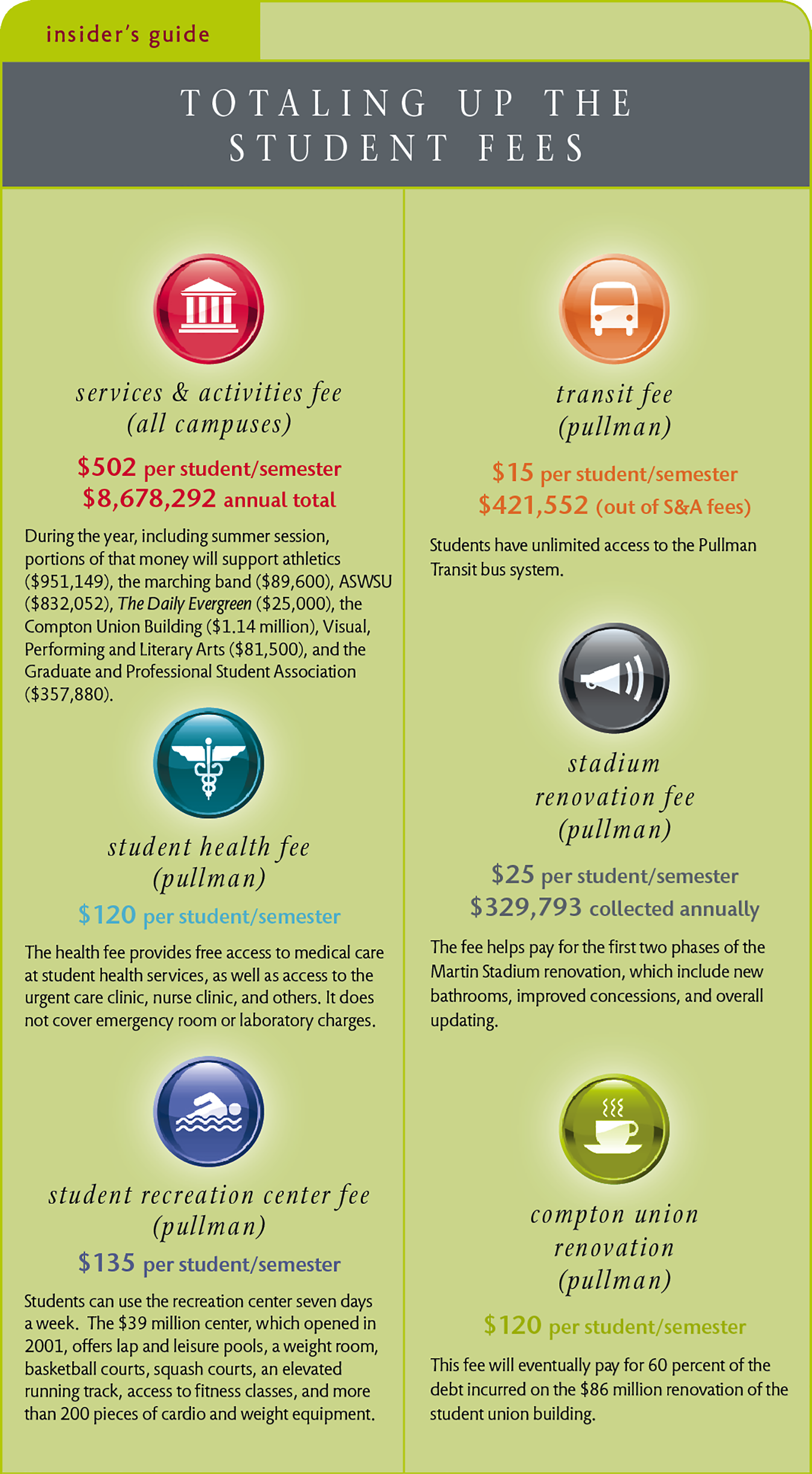

Totaling Up the Student Fees

Click on infographic for larger version

In the spring of 2008, the WSU Board of Regents set the Services and Activities Fees for the 2008-2009 academic year at $502 for all full-time students, an increase of 5 percent from the previous year. The sum doesn’t include fees for buildings and renovations (which students have voted to fund). Special course fees are an additional cost. In fall 2008 they range from $2 for an English class to $1,150 for Interior Design 277, an optional course that involves an out-of-state field trip.

SOURCE: WASHINGTON STATE UNIVERSITY